CGV: MicroStrategy’s Success Propels Corporate Balance Sheets into the Programmable Era

- Jul 11, 2025

- 10 min read

Published by: CGV Research

Authors: Cynic

Driven by the Trump administration's strategic pivot towards embracing crypto assets, the crypto reserves held by publicly listed companies are poised to surpass the $100 billion mark. This article systematically maps the global landscape of corporate crypto reserves, deeply analyzes the capital operation model centered on MicroStrategy, and explores the differentiated paths and potential risks of altcoin reserve companies. This "digital asset transformation" experiment, led by traditional corporations, is reshaping the future paradigm of corporate financial management.

Global Corporate Crypto Reserve Landscape

Geographical Distribution of Listed Companies: US-listed companies dominate with 65.2%, followed by Canada (16.9%), Hong Kong (7.9%), Japan (3.4%), and other markets (6.7%).

Cryptocurrency Composition: BTC accounts for 78% of reserves. ETH, SOL, and XRP holdings are similar, each around 5–6%. Companies holding other crypto assets make up the remaining 5%.

Value Distribution: BTC holds an absolute lead, representing 99% of the total reserve value. All other assets combined account for the remaining 1%.

Statistical analysis of the timing of companies' first announcements of strategic crypto reserves reveals distinct peaks and troughs, aligning closely with the cryptocurrency market's own bull and bear cycles.

Two Significant Peaks:

2021: 25 companies announced strategic reserves, primarily driven by rising Bitcoin prices and the MicroStrategy demonstration effect.

2025: 28 companies announced, marking a historic peak and showing increased acceptance of crypto as a corporate reserve asset.

Trough Characteristics:

2022–2023: Only 3 companies entered, reflecting the impact of the crypto bear market and regulatory uncertainty.

Companies continue to announce crypto reserves recently. The number of listed companies with crypto reserves is expected to exceed 200 this year, indicating sustained growth in crypto adoption within traditional industries.

Strategic Reserves, Capital Operations & Stock Performance

Current capital operation models for digital asset reserve companies can be categorized as follows:

Leveraged Accumulation Model: Companies with weak core businesses raise funds through debt or equity financing to buy crypto assets. Rising crypto prices boost net assets, driving up stock prices and enabling further financing, creating a positive feedback flywheel. Essentially, the company's stock becomes leveraged exposure to the crypto asset. If executed well, it can amplify stock price and net asset growth with minimal capital. Examples: MicroStrategy ($MSTR - BTC), SharpLink Gaming ($SBET - ETH), DeFi Development Corp ($DFDV - SOL), Nano Labs ($NA - BNB), Eyenovia ($EYEN - HYPE).

Cash Management Model: Companies with strong, non-crypto-related core businesses use surplus cash to purchase quality crypto assets for investment returns. Usually has no significant positive impact on stock price; may even cause declines due to investor concerns about neglecting the core business. *Examples: Tesla ($TSLA - BTC), Boyaa Interactive (HK0403 - BTC), Meitu (HK1357 - BTC+ETH).*

Operational Reserve Model: Companies directly or indirectly hold reserves due to crypto-related core operations (e.g., exchange needs, miners holding mined Bitcoin as reserves against business risks). Examples: Coinbase ($COIN - various), Marathon Digital ($MARA - BTC).

Among these companies, MicroStrategy stands out. It skillfully leveraged debt, transforming from a long-unprofitable software vendor into a Bitcoin whale with a market cap in the tens of billions. Its operational model warrants deep study.

MicroStrategy: The Textbook on Leveraged Crypto Reserve Operations

Five Years, Thirtyfold Rise: The Bitcoin Leverage Proxy

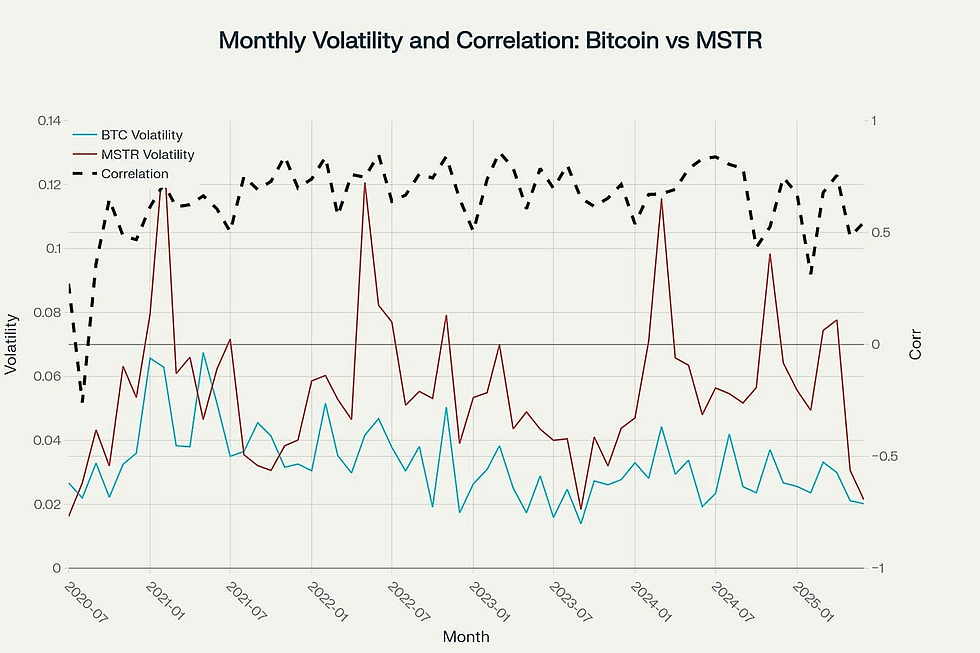

Since MicroStrategy announced its Bitcoin treasury strategy in 2020, its stock price ($MSTR) has exhibited a strong correlation with Bitcoin's price ($BTC), but with significantly higher volatility, as clearly shown in the chart below. From August 2020 to present, MSTR has risen nearly 30x, while Bitcoin itself has only risen 10x over the same period.

Monthly statistical analysis of volatility and correlation between Bitcoin and MSTR shows:

MSTR's price correlation with BTC mostly ranges between 0.6–0.8, indicating a strong relationship.

MSTR's volatility is consistently multiples higher than Bitcoin's.

Effectively, MSTR functions as a leveraged equity proxy for Bitcoin. This leverage attribute is further validated by market pricing: In June 2025, MSTR's 1-month call options implied volatility was 110%, 40 percentage points higher than Bitcoin spot volatility, reflecting a market-assigned leverage premium.

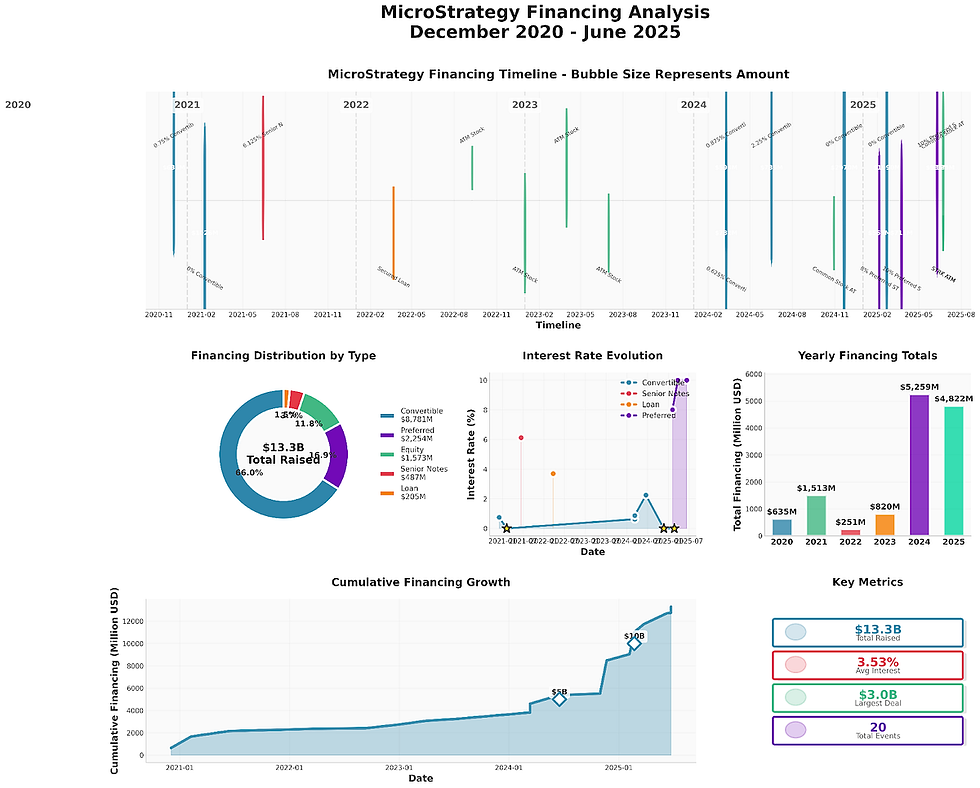

A Precision Capital Operation Machine

The core of the MicroStrategy model is acquiring funds at a low cost to buy Bitcoin. As long as Bitcoin's expected return exceeds the actual financing cost, the model remains viable.

MicroStrategy has created a matrix of capital instruments, transforming Bitcoin's volatility into a structural financing advantage. It employs multiple financing strategies, forming a self-reinforcing capital cycle. VanEck analysts describe it as a "pioneering experiment merging digital currency economics with traditional corporate finance."

MicroStrategy's capital operations have two core objectives: Controlling the debt ratio and increasing the Bitcoin per Share. Assuming long-term Bitcoin appreciation, achieving these goals enhances the stock's value.

Compared to collateralized loans (which face inefficiencies like 150% over-collateralization requirements, uncontrollable liquidation risks, and size limits), financing tools with embedded options like convertible bonds and preferred stock offer lower costs and less impact on the balance sheet structure. At-The-Market (ATM) common stock sales provide quick, flexible cash access. Furthermore, preferred stock is treated as equity, not debt, in accounting, further reducing the debt ratio compared to convertible bonds.

This complex matrix of capital instruments is highly favored by professional investors, enabling arbitrage based on differences in realized volatility, implied volatility, and other option pricing components. This also underpins strong demand for MicroStrategy's financing tools.

Analyzing quarterly Bitcoin holdings, debt levels, and major capital events reveals:

MicroStrategy combines various financing tools: Issuing convertibles and preferred stock during high BTC volatility/high stock premium bull markets to expand Bitcoin holdings.

Using ATM common stock sales during low BTC volatility/negative stock premium bear markets to prevent excessive debt ratios and cascading liquidation risks.

Reasons for preferring convertibles/preferred stock during high premium periods:

Delayed Dilution Effect: Direct ATM issuance dilutes existing shareholders immediately. Convertibles/preferred stock delay dilution via embedded conversion options.

Tax Efficiency: Preferred dividends (e.g., STRK's 8% rate) are 30% tax-deductible, reducing the effective cost to ~5.6%, below comparable corporate bond rates (~7.2%). Common stock financing offers no tax deduction.

Avoiding Reflexivity Risk: Large ATM programs signal perceived overvaluation by management, potentially triggering algorithmic selling.

Debt Ratio = Total Debt ÷ Total BTC Holdings Value

mNAV = Market Cap ÷ Total BTC Holdings Value

Due to its unique financing structure, when Bitcoin rises, MSTR rises more sharply, and significant debt gets converted to equity. In fact, since announcing Bitcoin purchases, MicroStrategy's total shares outstanding have increased from 100M to 256M (+156%).

Does this massive share dilution harm shareholder equity? Data shows that despite 156% share dilution since Q4 2020, the stock price has risen nearly 30x, meaning shareholder equity increased substantially. To better represent shareholder value, MicroStrategy introduced the Bitcoin per Share (BTC/Share) metric, making its continuous increase a core capital operation goal. The chart shows a long-term rising trend in BTC/Share, increasing tenfold from the initial 0.0002 BTC/Share.

Mathematically, when MSTR trades at a high premium to NAV (mNAV > 1), financing via potential equity dilution to buy Bitcoin can continuously increase BTC/Share. mNAV > 1 means each dollar raised buys more BTC than the current BTC/Share. While existing shares are diluted, the post-dilution BTC value per share still increases.

The Future Trajectory of MicroStrategy

The success of the MicroStrategy model hinges on three key factors: regulatory arbitrage, correctly betting on Bitcoin's rise, and superior capital operation skills. However, risks are embedded within these factors.

1. Legal & Regulatory Changes:

Competition from Investment Tools: When MicroStrategy first announced its strategy, Bitcoin spot ETFs were unavailable. Many institutions used MSTR as a proxy for Bitcoin exposure within compliance frameworks. Under the Trump administration's pro-crypto push, numerous compliant crypto investment tools (like spot ETFs) are emerging, narrowing the regulatory arbitrage window.

SEC Scrutiny on "Non-Productive Assets": Despite MicroStrategy's sophisticated debt management keeping its debt ratio lower than many peers of similar size, its debt is solely for investment, not business expansion. The SEC might reclassify it as an investment company, increasing capital adequacy requirements by 30%+ and compressing leverage capacity.

Capital Gains Tax: Taxing unrealized gains on corporate holdings (as proposed in the OBBB bill) would create massive cash tax liabilities for MicroStrategy. (Current rules tax only upon sale).

2. Bitcoin Market Dependency Risk:

Volatility Amplifier: Holding 2.84% of all Bitcoin means MSTR's stock volatility amplifies Bitcoin's volatility during market swings, putting heavy downward pressure on the stock in bear cycles.

Irrational Premium: MSTR's market cap has consistently traded at a >70% premium to its Bitcoin NAV, largely driven by irrational market expectations of Bitcoin's rise.

3. Ponzi-like Structural Risk of Debt Leverage:

Convertible Bond Refinancing Reliance: The cycle of "issue new debt → buy BTC → boost stock price → issue more debt" exhibits double Ponzi characteristics. If Bitcoin prices don't rise sufficiently to support the stock when large bonds mature, new debt issuance falters, triggering a liquidity crisis (rollover risk). If BTC falls below convertible strike prices, forced cash repayment occurs (conversion price inversion).

Lack of Stable Cash Flow: With no stable operational cash flow and reluctance to sell Bitcoin, MicroStrategy relies almost entirely on equity issuance (conversions, ATM) for debt servicing. If the stock or Bitcoin price falls significantly, financing costs soar, potentially closing funding channels or causing severe dilution, jeopardizing continued accumulation or operational cash flow.

Long-term, during a risk asset downturn, multiple risks could converge, creating a technical risk transmission mechanism and triggering a death spiral:

Another possibility is regulatory intervention, converting MicroStrategy into a Bitcoin ETF or similar product. Its 2.88% Bitcoin holdings pose systemic risk if forced into a fire sale; conversion would be safer. While large, its holdings wouldn't be exceptional among ETFs. Furthermore, the SEC's July 2, 2025, approval of Grayscale's Digital Large Cap Fund conversion into a multi-asset (BTC, ETH, XRP, SOL, ADA) ETF demonstrates the feasibility.

The Altcoin Reserve Experiment: $SBET & $DFDV Case Studies

Valuation Regression Analysis: Sentiment-Driven to Fundamentals-Based Pricing

$SBET's Volatility Path & Stabilization Signals

Cause of Surge & Crash:

May 2025: $SBET announced a $425M PIPE financing to acquire 176,271 ETH (~$463M at the time), becoming the largest corporate ETH holder. Stock surged 400% intraday.

Subsequent SEC filings revealed PIPE investors could immediately resell shares, triggering panic selling over dilution fears. Stock plunged 70%.

Ethereum co-founder Joseph Lubin ($SBET Chairman) clarified "no shareholder sales planned," but sentiment was damaged.

Valuation Recovery Signs (as of July 2025):

Stock stabilized around $10. mNAV ~1.2 (post-PIPE dilution implied mNAV ~2.67).

Stabilization drivers:

ETH Holding Appreciation: Added $30.6M to buy 12,207 ETH. Total holdings: 188,478 ETH (~$470M), ~80% of market cap.

Staking Rewards Realized: Earned 120 ETH via Liquid Staking Derivatives (LSDs).

Improved Liquidity: Average daily trading volume reached 12.6M shares; short interest fell to 8.53%.

$DFDV's Ecosystem Integration Premium

Compared to $SBET, while $DFDV also exhibits high volatility, its stock demonstrates stronger downside support. Despite experiencing a 36% single-day drop, $DFDV remains up 30x from pre-transformation levels. This resilience stems partly from its low pre-transformation market cap and, crucially, its business diversity, particularly infrastructure investments providing additional valuation support.

Valuation Support from SOL Reserves:

$DFDV holds 621,313 SOL (~$107M), generating three income streams:

SOL price appreciation (~90% of holding value).

Staking rewards (5%-7% APY).

Validator commissions (charged to ecosystem projects like $BONK).

PoW vs. PoS: The Impact of Staking Rewards

Native staking of PoS cryptocurrencies like ETH and SOL provides annual yields. While this yield might not directly impact traditional valuation models, liquid staking enhances capital operation flexibility.

Bitcoin (PoW) has no yield mechanism but is fixed-supply with declining inflation (~1.8%), emphasizing scarcity.

PoS tokens generate yield via staking. If staking APY exceeds token inflation, staked assets gain nominal value. Current SOL staking APY is 7–13% vs. inflation ~5%; ETH staking APY is 3–5% vs. inflation <1%. Current ETH/SOL staking provides extra return, but inflation vs. reward dynamics need monitoring.

Staking rewards are token-denominated and cannot directly translate into secondary market buying pressure to boost token prices.

Liquid staking allows using the liquid staked tokens (e.g., stETH, stSOL) in DeFi (e.g., as collateral for loans), significantly improving capital flexibility (e.g., DFDV issued DFDVSOL).

Validation of $MSTR Success Factors for Altcoin Reserve Companies

1. Regulatory Arbitrage: Window Narrowing

ETF approvals have accelerated significantly. Multiple institutions are filing for various crypto ETFs; approval is a matter of time. While altcoin reserve company stocks/bonds still meet some investor demand before more complex, token-specific instruments emerge, the regulatory arbitrage window is closing.

2. Token Appreciation Bet: Altcoin Performance Uncertain

Bitcoin ("digital gold") enjoys global liquidity consensus as a reserve asset. ETH/SOL lack equivalent status and are primarily viewed as utility assets.Altcoins underperformed Bitcoin significantly in 2024–2025:

Bitcoin dominance rose steadily in 2024, reaching ~65%.

Historically, "altcoin seasons" followed Bitcoin peaks, but altcoin performance lagged this cycle.

When Bitcoin hit new ATHs, ETH and SOL remained below 50% of their own historical highs.

3. Capital Operation Skills: Enhanced Flexibility

Compared to Bitcoin reserve companies, altcoin reserve companies can engage more deeply in blockchain ecosystems to generate cash revenue and utilize DeFi for higher capital efficiency.

Examples:

$SBET (Chaired by Consensys founder) potential in wallet, blockchain, staking services.

$DFDV partnered with Solana's largest Meme coin $BONK to acquire validator networks (commissions = 34% of Q2 revenue).

$DFDV packaged staking rewards as DeFi-tradable dfdvSOL.

$HYPD (ex-Eyenovia $EYEN) staking/lending $HYPE, expanding node ops/affiliate programs.

$BTCS (Ethereum node/staking provider) stakes $ETH, uses LSTs and BTC as Aave collateral for low-cost funding.

In summary, narrowing regulatory arbitrage and uncertain token appreciation will force altcoin reserve companies to innovate. They must integrate deeply into on-chain ecosystems and build cash flow through ecosystem activities to enhance resilience.

While MicroStrategy uses sophisticated capital tools to transform Bitcoin into "volatility leverage," altcoin reserve companies are attempting to solve their valuation dilemma through DeFi-enabled operations. However, the narrowing regulatory arbitrage window, differences in token consensus strength, and inflation concerns inherent in PoS mechanisms ensure this experiment remains fraught with uncertainty. As more traditional companies enter the fray, strategic crypto reserves will likely evolve from aggressive bets towards rational allocation. Their ultimate significance may lie not in short-term arbitrage, but in propelling corporate balance sheets into the programmable era.

As Michael Saylor stated: "We're not buying bitcoin, we're building a treasury system for the digital age." The ultimate test of this experiment will be the balance sheet's resilience during a Bitcoin bear market, facing the double squeeze of declining asset values and amplified stock volatility. This is the critical question traditional enterprises must answer before joining the movement.

----------------------

About Cryptogram Venture (CGV):

CGV (Cryptogram Venture) is a crypto investment institution headquartered in Tokyo, Japan. Since 2017, its fund and predecessor funds have participated in investments in over 200 projects. Since 2022, CGV has invested in and incubated the licensed Japanese yen stablecoin JPYW, making an early move in the crypto stablecoin sector. Starting in 2024, CGV has expanded into the tokenized equity and RWA markets, participating in private placements of projects such as Nabate (NA) and Victory Securities (8540.HK). Currently, CGV also has branches in locations such as Hong Kong and Silicon Valley.

Disclaimer:

The information and materials introduced in this article are sourced from public channels, and our company does not guarantee their accuracy or completeness. Descriptions or predictions involving future situations are forward-looking statements, and any advice and opinions provided are for reference only and do not constitute investment advice or implications for anyone. The strategies our company may adopt could be the same, opposite, or unrelated to the strategies readers might speculate based on this article.

Comments